For a large proportion of UK law firms, the financial year ending in 2021 was one of their most profitable in the last 30 years.

A perfect set of circumstances existed: law firms saved substantial expenses from offices lying dormant, funding and support was readily available from the Government. Within firms there was great anxiety around the risks of redundancies. People were housebound with limited options to occupy their time and of course people wanted to 'look busy' so chargeable time was strong. At the same time due to the situation the UK faced during the Covid-19 pandemic the demand for legal services was also ironically very strong.

These ‘perfect’ set of circumstances largely drove an all-time high in terms of financial results reported in 2021.

The decline of law firm productivity

In the financial years that followed in 2022 to 2024 there was a decline in the level of productivity in law firms.

There are various key performance indicators (KPIs) available to firms to monitor productivity and core profit margins. Chargeable hours, fees per fee earner and people costs as a proportion of earned income (People costs) are the most common KPIs.

We do not cite gross or net profit margins on this list because whilst these are commonly quoted, they are affected by ownership decisions (the number of Equity Partners or shareholders/owners a firm has) between accounting years and between different firms. These decisions impact the costs in the profit and loss account and can distort comparison.

People costs, which builds in a notional salary for owners alongside direct payroll costs conversely tells us more reliably what it costs to generate earned income in terms of full direct costs.

In our experience most law firms over the last 30 years have been reporting a result here of between 55% and 65% with the most common long-term level being around 61%.

In 2021 this KPI dipped significantly and we were much more commonly seeing results of 56% and 57% amongst firms – keeping in mind a 1% shift in this KPI makes a large difference to profitability.

However, if we look at the results of firms in 2022 to 2024, we will commonly find that this KPI was worsening and by 2024 it was common to see a result of 64% or 65% - worse than the longer-term average of 61%.

During this period there were a couple of significant background factors in the legal sector.

Chargeable hours were declining

The short-term boost from COVID in terms of productivity where there was anxiety over job security faded. Law firms were locked into arrangements and a culture of fee earners working remotely. It would be an unpopular comment to link these factors but as independent statements data shows that chargeable hours have declined post COVID compared to pre-COVID and coterminously working from home has expanded.

PwC Legal survey - Top 51 – 100 firms

| Chargeable hours p.a. |

Category/ Average | 2025 | 2024 | 2020 |

3-5 years PQ | 1,127 | 1,154 | |

6-8 years PQ | 1,088 | 1,126 | |

Fixed Share Members | 812 | 832 | |

1-9 years PQ | 1,097 | | 1,139 |

Law Society survey

| 2024 | 2023 | 2022 | 2021 |

Average chargeable hours p.a. | 773 | 793 | 841 | 861 |

Salary Inflation

Attracting and retaining talent is almost always cited as one of the largest challenges that law firms face. In 2022 demand for talent exploded in the backdrop of high demand for legal services. We all remember the headlines for the increasing rates for newly qualified and of course there was a similar experience across many levels of people costs in firms.

The table below illustrates the levels of income growth compared with employee cost growth that we commonly saw in these 3 years across the sector.

| Income growth achieved | Employee cost increase | Background peak inflation |

2022 | 5%-8% | 10%+ | 8% |

2023 | 8%-10% | 15%+ | 8% |

2024 | 8%-12% | 10%+ | 3% |

The result of these two factors working in tandem resulted in the deterioration of the People cost KPI and core profitability in law firms in this period.

Less chargeable time went on the clock, the salaries went up significantly and this was not counteracted by a full inflationary increase in rates charged to clients.

NatWest Legal Survey

| 2025 | 2024 |

People costs as a % of earned income | 64% | 65% |

The stability of profitability

Having considered productivity, the next consideration is profitability. Excluding the newer ownership models in the legal sector, most firms are still partnerships or companies where the owners work in the business day today; so, the most common profitability measure used is PEP (profits per Equity Partner / owner).

PEP reported in 2021 was amongst the highest result for law firms in the last 30 years. However, given the deterioration in margins in 2022 to 2024 we would have expected perhaps to see a significant decline in PEP for those years.

The results however show a different picture and many firms in that period have shown solid profitability – often lower than 2021 but still above longer-term averages and certainly not reflective of the erosion in margins.

NatWest Legal Survey – Median PEP

| 2025 (£’000) | 2024 (£’000) |

All firms | 340 | 274 |

Small firms (<£5m turnover) | 204 | 162 |

Large firms (>£10m turnover) | 372 | 284 |

Other surveys – Median PEP

| 2025 (£’000) | 2024 (£’000) | 2021 (£’000) |

Law Society | 249 | 210 | 203(*) |

The Lawyer (top 51-100) | 408 | 390 | 555 |

(* -UK inflation adjusted to 2025 this would become £249k)

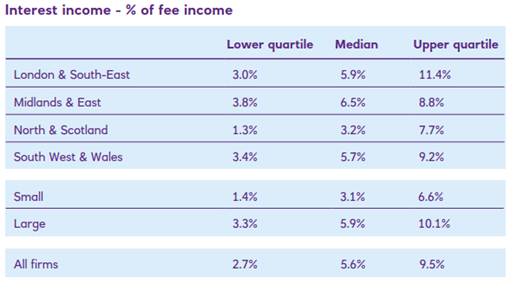

When you consider the wider profit and loss account of many law firms over this period the most notable change is profits on client interest receipts.

As shown by data from the 2025 NatWest Legal survey below these reached a median of 5.6% of earned income and 21% of PEP amongst a cross section of firms by 2025 and for the upper quartile 25% of firms reported that interest income presented 35% or most of their profits (PEP).

The evidence perhaps suggests that in the intervening years the increase in client interest profits provided a significant buffer to many law firms enabling them to continue to earn strong / healthy profits in the backdrop of declining productivity and margins.

This set of circumstances has allowed: -

Consumers to benefit from lower inflation in their legal costs.

Fee earner productivity to decline and be relatively unchallenged.

Fee earner salary levels to escalate to keep pace with the market without challenge.

Law firms to avoid the difficult conversations with clients on rate rises and fee earners on productivity.

What actions are law firms taking?

During mid to late 2024 we started to notice a change of approach in firms. The declining margins (increasing People cost KPI and reducing chargeable hours KPIs) started to become more headline discussions in firms.

Board discussions which in the period 2021 to 2024 were centred around challenges of recruitment and retention to meet client demand shifted in mid-2024 to focusing on productivity.

In the top 150 firms our experience is that this shift arose in part from the pressures that were starting to be exerted on PEP levels from increased I.T investment needs and at the same time the KPIs were sounding the decline in productivity.

Outside the top 150 firms however the most common factor which mustered a call to action was the signal from the SRA in late 2024 to challenge the ability of law firms to hold client money or retain profits from client interest. Many firms were cognisant of the degree to which profits were being propped up by interest income, but few were taking action until this point. Naturally the Ministry of Justice consultation in 2026 has further fuelled concern for law firms in this area.

Reflecting on the results of law firms in the period 2022 to 2025 they should have been exceptional profit results for many firms – because of the return of interest income profits which were absent since 2008.

So, where have law firms been focusing their productivity push?

Time capture – Getting time recording disciplines at the front of fee earners minds and on the agenda for those monitoring performance. This has included ensuring fee earners gain a better understanding that time recording is undertaken to primarily assess what it costs to undertake work and to educate future pricing – and that it’s not just a process to bill the client.

Scoping – Once firms are confident about the quality of time capture the next challenge is to ensure that their client care letter and general engagement terms give them the contractual right to bill the client for the time they spend. Many firms have approached this by a combination of fee earner training but also through the creation of standardised scoping documents for common pieces of work and subsets of work to help fee earners better manage the scoping process.

Client communication – The final, and most difficult part of this journey for firms is instilling in its people that continual discussion of scoping and costs with clients during a matter is a key part of the service experience.

In our experience many firms are only part way through this journey, and we have seen much more work being undertaken in these areas in the 2026 financial year end.

However, it was apparent to us both through our own experience in the sector and through various national surveys, that the sector did see some small improvements in productivity (through People cost KPI reductions and small improvements in average chargeable hours in 2025). It is too early to say whether this has been because of the actions on the above issues in firms and 2026 results may start to explain the position further for us.

There is also evidence that firms have been adjusting their remote working policies with increasing numbers of firms requiring more office-based time to be delivered.

Is Law firm management only about productivity?

Another important dynamic is the ownership structure.

If we consider the profit generation model in law firms this is largely centred around – average chargeable hours, average rate charged, average recovery rate achieved and an allowance for overheads per £1 of revenue (let’s call this the size of the cake).

The other key element of the model is the gearing – that is the number of fee earning individuals per owner (let’s call this the number of slices).

In running a law firm, there are many levers that can be tweaked in terms of trying to improve the ‘size of the cake.' These mainly revolve around the general management of fee earners and client matters but the key issue here is that these tweaks are often across large volumes of people and clients and so sometimes only a very modest improvement can make a significant difference to the 'size of the cake.'

Conversely, where a firm’s gearing is concerned there are relatively few options or levers to improve a situation – for example if the gearing is too low (so too many Equity Partners / owners) given the size of the firm, in practical terms the main two options to improve this are:

Both of course are difficult challenges, often less readily implemented than changes needed to ‘improve the size of the cake.’

Considering People costs KPIs for instance will give evidence of the marginal profitability of a team – however understanding how many Equity owners that team needs to ‘feed’ in terms of PEP is also an important dynamic.

For example – a private client team with a strong People cost KPI of say 59% may look good at a margin level but if the gearing is only a poor result at 4.5 fee earners per owner, then the absolute profit contribution per Equity owner to the overall firm may still be poor.

Conversely, perhaps a family and care team with a poor People cost KPI result of 67% might only have one Equity owner producing a gearing result of 8.5 fee earners per owner. Consequently, although the margin of the work is 'poor' the contribution to the Equity Partner profit pot is strong.

For the family team, the issue may be around managing the margin – so time capture, pricing, mix of skills, work delegation – matter management. In the private client team however, the issues are different – we may be looking at a longer-term strategy of simply reducing Equity owners, possibly simply on retirements or maybe through growth without proportionate increases in Equity owners.

Considering the actions we have seen across the legal sector we would be expecting firms, over the next few years, to be seeking to return their core profit margins to the longer-term average levels.